Singapore

Singapore Hongkong

Hongkong Global

Global Group

Group Log In

Log InReport by James Ooi/uSMART Market Strategist

Summary: In the article, analysts believe that the US stock market may experience a relatively calm week, but investors still need to pay attention to to the possibility of a downgrade in the US sovereign credit rating. The market rally this year has lacked breadth, and bond traders are skeptical about the optimistic sentiment in the stock market. However, underperforming sectors like healthcare, energy, and industrials have started to catch up recently, potentially driving the S&P 500 higher. The Federal Reserve's stance seems slightly less hawkish, and while the latest employment data may keep rates unchanged in June, there's a 53% chance of a rate hike in July. With limited short-term upside potential and high valuations, investors are advised to exercise caution in the US stock market.

.jpg)

About James:

James Ooi/ uSMART Market Strategist

Over 13 years of experience in buy-side and sell-side of capital markets

Former Fund Manager of renowned asset management firm

Focus on fundamental analysis and macro-outlook for US & Singapore markets

SGX Academy trainer

This Week’s Market Outlook

This week's significant economic data in the United States includes the release of the ISM Services PMI on Monday, as well as the Unemployment Claims report scheduled for Thursday. Due to the lack of major economic data, the US equity market may have a relatively quiet week.

After President Biden signed the debt ceiling bill to avert a first-ever US default, the US debt crisis was temporarily alleviated. However, investors still need to pay attention to the possibility of a downgrade in the US sovereign credit rating. Fitch Ratings, a leading provider of credit ratings, stated on Friday that they may still downgrade the U.S.’s credit rating.

Looking back at 2011 (Figure 1), both parties in the United States went through a series of struggles over the debt ceiling issue. Although they eventually reached an agreement, the Standard & Poor's decision to put the US sovereign credit rating on negative watch and subsequently downgraded it from AAA to AA+ resulted in a nearly 18% drop in the S&P 500 index.

Figure 1: S&P 500 during the 2011 debt ceiling drama

Source: uSMART, Tradingview

Source: uSMART, Tradingview

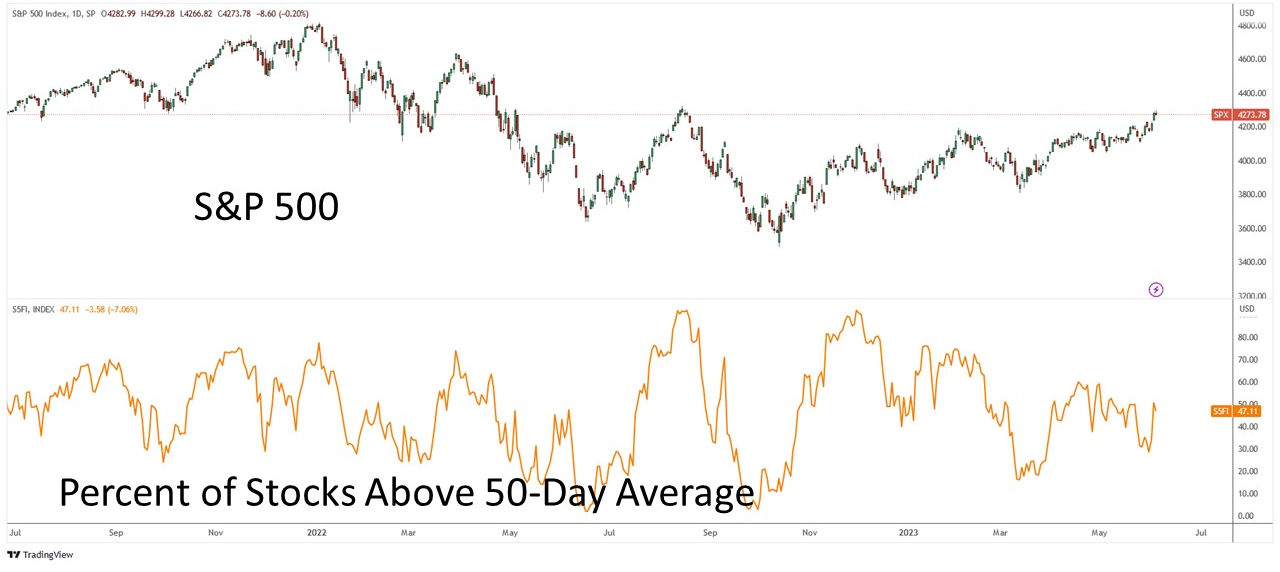

The S&P 500 is currently near its yearly high; however, only 43% of stocks within the S&P 500 are currently trading above their 50-day moving average. This indicates that the year-to-date rally lacks market breadth (Figure 2).

Figure 2: S&P 500 Stocks Above 50-Day Average

Source: uSMART, Tradingview

Source: uSMART, Tradingview

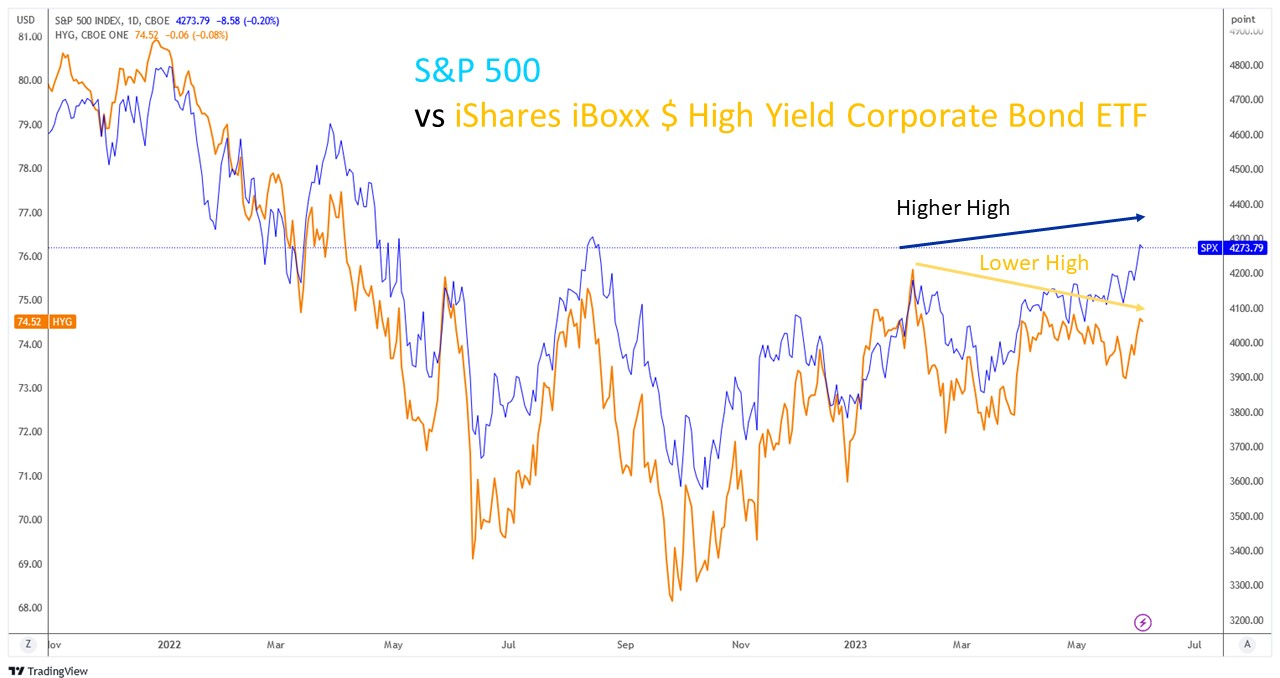

HYG (iShares iBoxx High Yield Corporate Bond ETF) typically moves in tandem with the S&P 500 (Figure 3). However, HYG has not followed the S&P 500 in creating higher highs this year. This suggests that credit traders are still skeptical of the stock traders' optimism and are not fully convinced by the upward trend.

Figure 3: S&P 500 vs iShares iBoxx $ High Yield Corporate Bond ETF

Source: uSMART, Tradingview

Source: uSMART, Tradingview

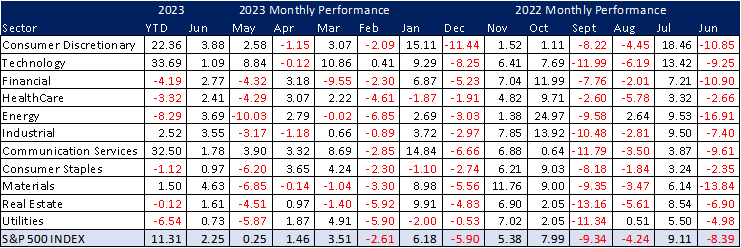

Some underperforming sectors, such as healthcare, energy, and industrial sectors, have recently started to catch up in terms of returns (Figure 4). If funds flow into other sectors, the S&P 500 has the potential to rise further. The S&P 500 index has delivered a return of 2.25% month-to-date. However, in June 2022, due to seasonality, the S&P 500 index experienced an 8% decline.

Figure 4: S&P 500 Monthly Return

Source: uSMART, Bloomberg, 5 June 2023

Source: uSMART, Bloomberg, 5 June 2023

Conclusion

The S&P 500 and Nasdaq-100 have returned 12.13% and 33.59% year-to-date, respectively.

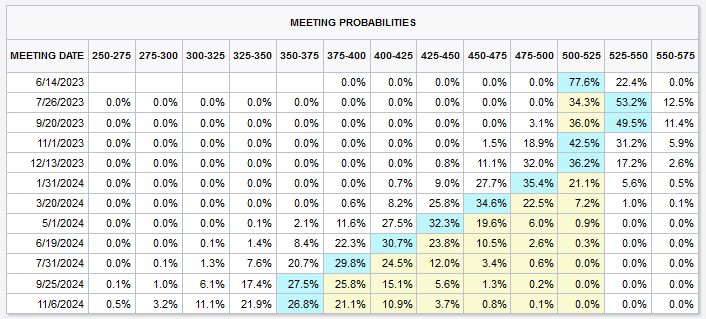

In May, the non-farm payroll reached 339,000, exceeding expectations of 190,000. However, the unemployment rate stood at 3.7%, higher than the expected 3.5%. Recently, the Federal Reserve appears slightly less hawkish, and we believe that the recent employment data is just soft enough for the Fed to justify keeping interest rates unchanged in June. However, according to CME FedWatch (Figure 5), there is approximately a 53% probability of another rate hike in July.

Figure 5: CME Fedwatch

Source: CME Fedwatch

Source: CME Fedwatch

There may be limited room for further upside in the US equity market, especially considering the relatively high valuations of many individual stocks. Therefore, we still urge investors to adopt a relatively cautious approach towards the US stock market.

Currently, there are several high-quality companies, such as Apple, Amazon, Visa, Tesla, Costco, and Microsoft, that continue to demonstrate strong long-term EPSgrowth potential. Investors may consider gradually establishing long-term positions in these companies. Additionally, investors can also explore ETFs like SPY, QQQ, and SUSA to capture some market returns.

Follow us

Find us on Twitter, Instagram, YouTube, and TikTok for frequent updates on all things investing.

Have a financial topic you would like to discuss? Head over to the uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimer:

This article is intended for general circulation and educational purpose only and does not take into account of the specific investment objectives, financial situation or particular needs of any particular person. You should seek advice from a financial adviser regarding the suitability of the investment products mentioned. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product in question is suitable for you.

Past performance figures as well as any projection or forecast used in this article, are not necessarily indicative of future performance of any investment products. Your investment is subject to investment risk, including loss of income and capital invested. The value of the investment products and the income from them may fall or rise. No warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of this article. Overseas investments carry additional financial, regulatory and legal risks, you should do the necessary checks and research on the investment beforehand.

The information contained in this article has been obtained from public sources which the uSMART Securities (Singapore) Pte Ltd (“uSMART”) has no reason to believe are unreliable and any research, analysis, forecast, projections, expectations and opinion (collectively “Analysis”) contained in this article are based on such information and are expressions of belief only. uSMART has not verified this information and no representation or warranty, express or implied, is made that such information or Analysis is accurate, complete or verified or should be relied upon as such. Any such information or Analysis contained in this presentation is subject to change, and uSMART, its directors, officers or employees shall not have any responsibility for omission from this article and to maintain the information or Analysis made available or to supply any corrections, updates or releases in connection therewith. uSMART, its directors, officers or employees be liable for any or damages which you may suffer or incur as a result of relying upon anything stated or omitted from this article.

Views, opinions, and/or any strategies described in this article may not be suitable for all investors. Assessments, projections, estimates, opinions, views and strategies are subject to change without notice. This article may contain optimistic statements regarding future events or performance of the market and investment products. You should make your own independent assessment of the relevance, accuracy, and adequacy of the information contained in this article. Any reference to or discussion of investment products in this article is purely for illustrative purposes only, is not intended to constitute legal, tax, or investment advice of any investment products, and must not be construed as a recommendation, an offer or solicitation for the subscription, purchase or sale of the investment products mentioned. This article does not create any legally binding obligations on uSMART. uSMART, its directors, connected persons, officers or employees may from time to time have an interest in the investment products mentioned in this article.